Doug Hutchinson

Doug Hutchinson

401k Withdrawal Rules: Know Before You Cash Out

When you leave a job — to retire, pursue other opportunities, or due to termination — you’ll have the option to cash out your 401(k). Receiving a big...

Unexpected illness, an emergency home repair, or job loss can create financial turmoil. In the midst of a crisis, withdrawing money from your 401(k) or 403(b) may seem like a good idea. That money is just sitting around anyway and you have plenty of time to pay yourself back…right?

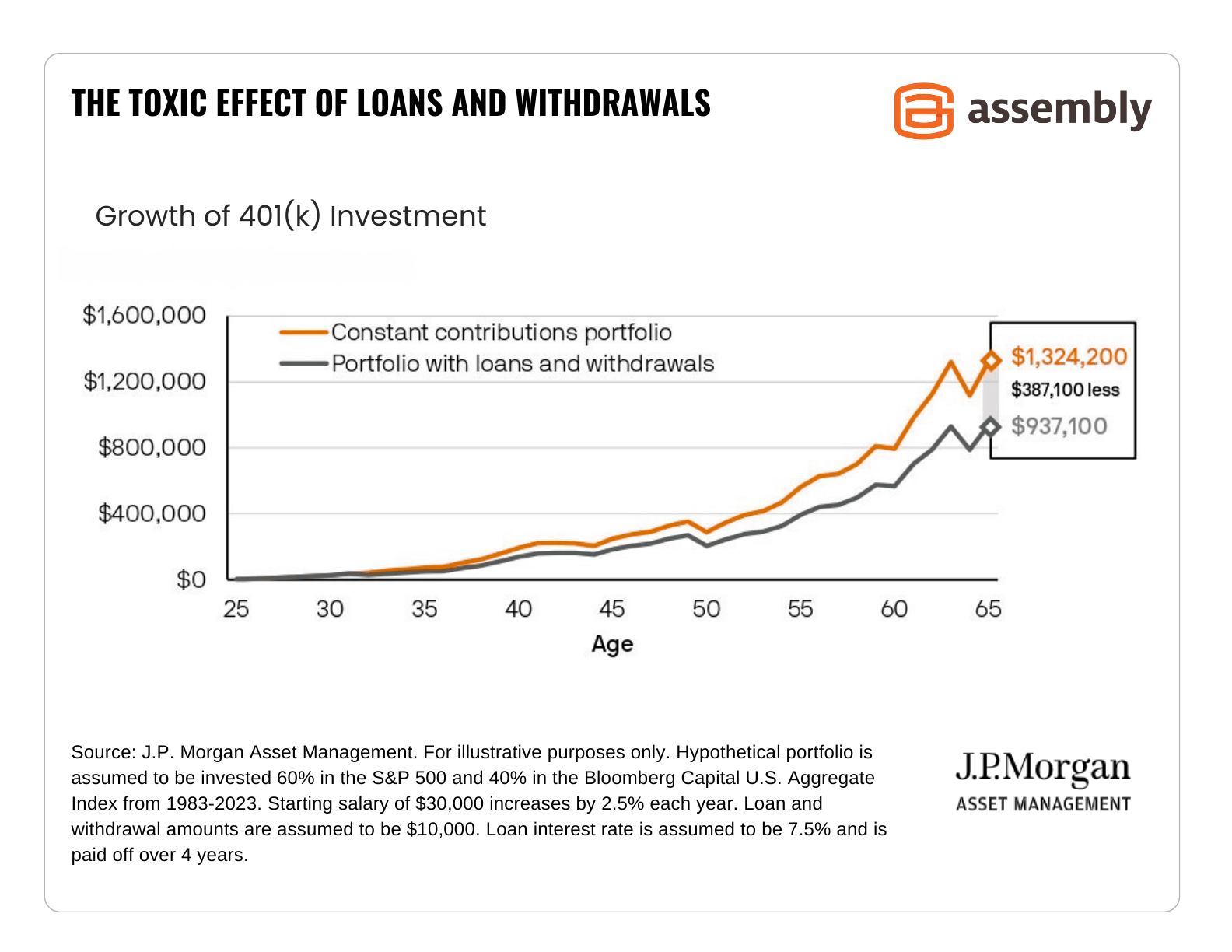

Withdrawing money from your retirement account may solve a short-term problem, but there are long-term consequences — as the charts in this article illustrate. Before you make any money moves, make sure you understand the negative effects of early withdrawals and 401(k) loans and consider other ways to meet an immediate financial need.

Emergency expenses and credit card debt are the top three reasons people borrow from their 401(k) or withdraw money early. Some would argue that paying off a high-interest credit card using money from your retirement account is a good idea. But withdrawing money from your 401(k) before the age of 59 ½ is generally a bad idea because of the penalties and taxes. A 401(k) loan may be a worthwhile option for some, but it comes with significant drawbacks.

-Plan-Loans-and-Withdrawals-Chart.png)

Before delving into all the pros and cons, let’s define the difference between a 401(k) loan and an early withdrawal.

-Chart.png)

-Chart.png)

Some retirement plans allow you to take money out of your retirement account sans penalty to cover emergency medical expenses, funeral expenses or to prevent foreclosure on your primary residence. The penalty is only waived if “the employee couldn't reasonably obtain the funds from another source” and you still have to pay income tax on the amount withdrawn. Learn more about hardship withdrawals on the IRS website.

Additionally, Section 115 of the SECURE 2.0 Act allows emergency distributions of up to $1000 penalty-free. Distributions can be made from a 401(k), 403(b) or 457(b) account to address an immediate need. You don’t have to pay yourself back, but if you don’t, no additional emergency withdrawals are allowed for three years.

The best way to avoid taking money out of your retirement savings is to establish an emergency fund. Ideally, you should have enough cash or other liquid assets to cover several months of living expenses. Your age, family size and risk for common financial challenges should be considered. A financial planner can help you calculate the size of your safety net.

If you have significant equity in your home, a Home Equity Line of Credit (HELOC) might be a good option. HELOCs often have lower interest rates than credit cards or personal loans.

A third, less attractive option is to take money out of a Roth IRA or Roth 401(k) if you have one. Because contributions go in after tax, you can withdraw them tax and penalty-free. Note: only contributions not earnings may be withdrawn without taxes or penalties in most cases if you’re under 59 ½ .

Generally speaking, no. But if you have significant high-interest debt and no other options, taking a loan from yourself is better than giving money to creditors or facing bankruptcy. A financial advisor can review your situation and offer personalized recommendations.

Questions? Our friendly and experienced advisors are happy to help. Contact us online or give us a call at (415) 541-7774.

Related Reading:

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

When you leave a job — to retire, pursue other opportunities, or due to termination — you’ll have the option to cash out your 401(k). Receiving a big...

As we age, we accumulate things: workout equipment, kitchen gadgets and 401(k) accounts from different jobs. The workout equipment and gadgets may be...

About 40% of U.S. workers will lose their job at some point in their career. Being laid off can leave you feeling rejected, sad, or even angry — even...