Xander Zabetian

Xander Zabetian

Year-End Financial Planning Checklist

With the year coming to a close, now is a good time to do an annual review of your financial health. Here are 10 financial planning items to review...

Diversification is one of the most effective strategies for managing risk and improving long-term investment outcomes. By choosing investments across a variety of different asset classes, investors can reduce volatility and improve their chances of steady returns, even in uncertain market conditions. No strategy can completely eliminate risk, but diversification has consistently proven to be a key driver of portfolio stability and resilience, as seen throughout this article.

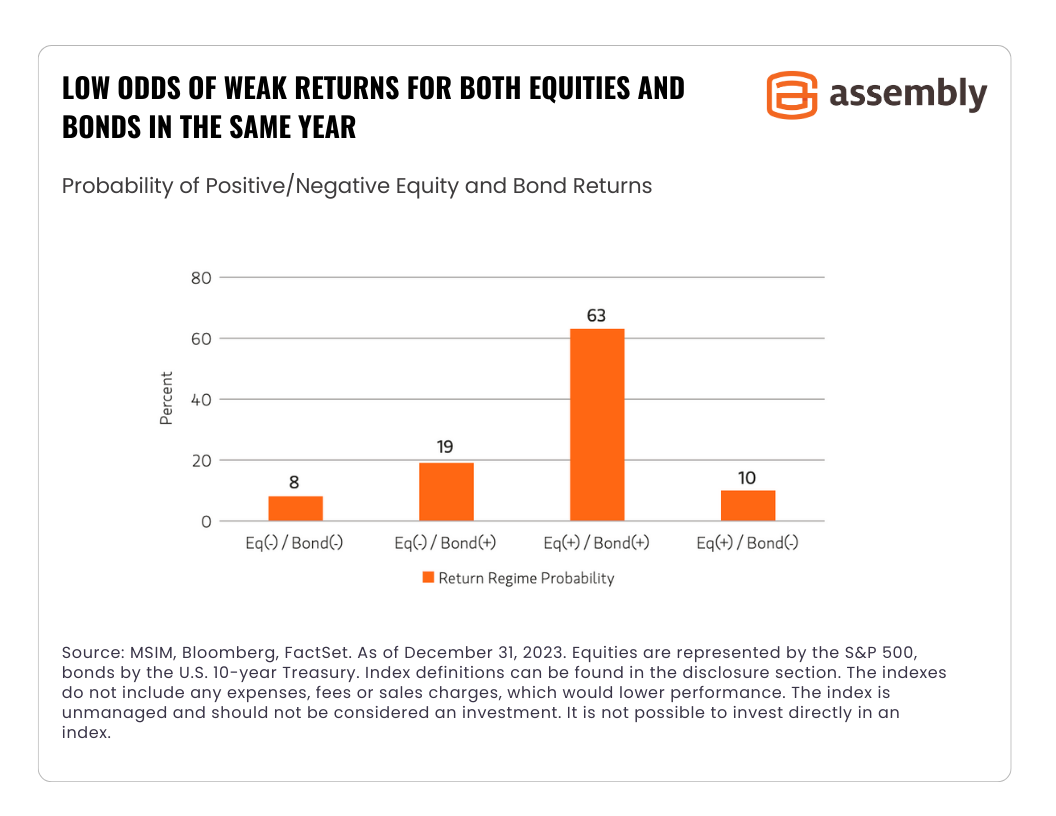

A well-diversified portfolio combines assets that react differently to economic conditions. The stock market and bond market often react differently to inflation, corporate earnings reports and interest rate changes. By holding a mix of stocks and bonds investors can minimize negative impacts to their portfolio. For example:

Bonds have historically served as a hedge against stock market downturns. As seen in the graph below, when stock markets face headwinds, bonds tend to perform better and provide a cushion against the negative impact.

You may remember both equities and fixed income experienced declines in 2022. But when making investment decisions, it’s important to look at the bigger picture and not focus on a single year. A diversified portfolio generally reduces the risk of large losses from any one asset class. We will discuss 2022 a bit more later.

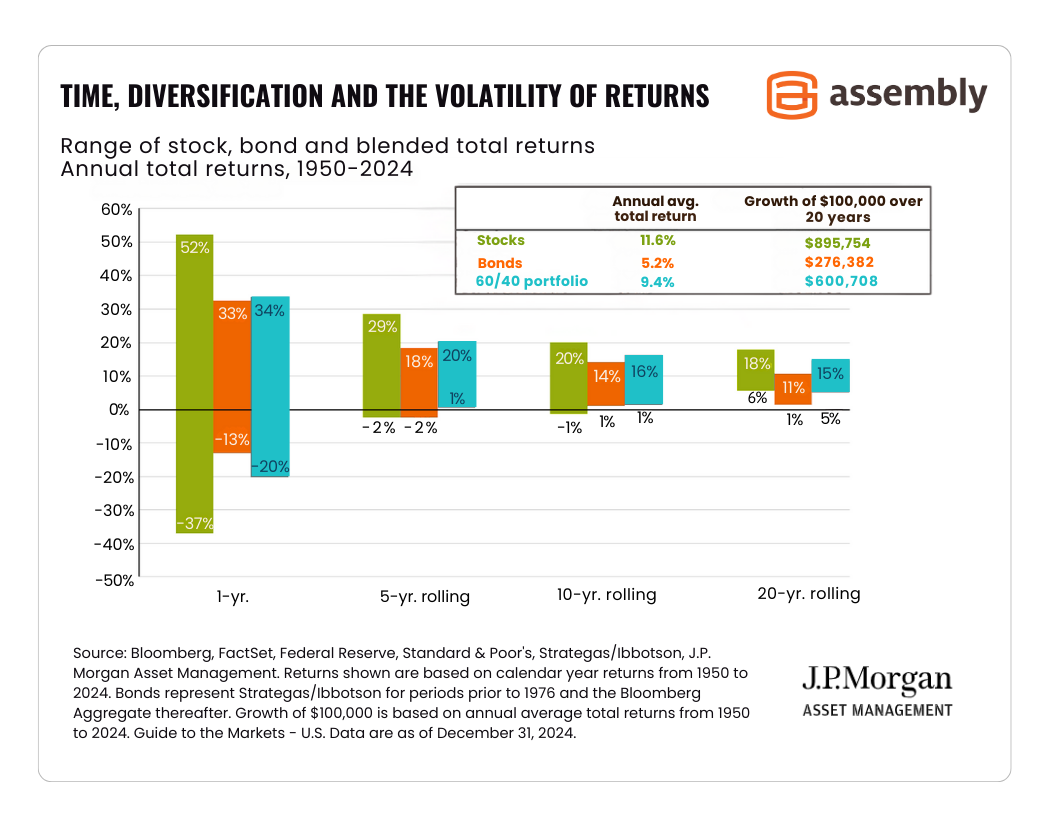

Historically, diversified portfolios tend to provide steadier returns over the long run. For example, a portfolio invested entirely in equities may experience significant growth in a strong stock market but also suffer steep losses during downturns. On the other hand, a diversified portfolio that includes fixed income can help reduce these extreme fluctuations.

One clear example of diversification in action is the 60/40 portfolio – an allocation of 60% equities and 40% fixed income. This portfolio has demonstrated steady performance over time. An analysis of a 5-year rolling annual total return since 1950 shows the portfolio's minimum return of around 1%, as seen in the graph below.

This is a marked contrast to equity-only portfolios, where the worst annual return over the same period dips into negative territory. While historical performance does not guarantee future results, the consistent track record of the 60/40 strategy suggests that diversification is an effective tool for managing risk while still capturing meaningful returns.

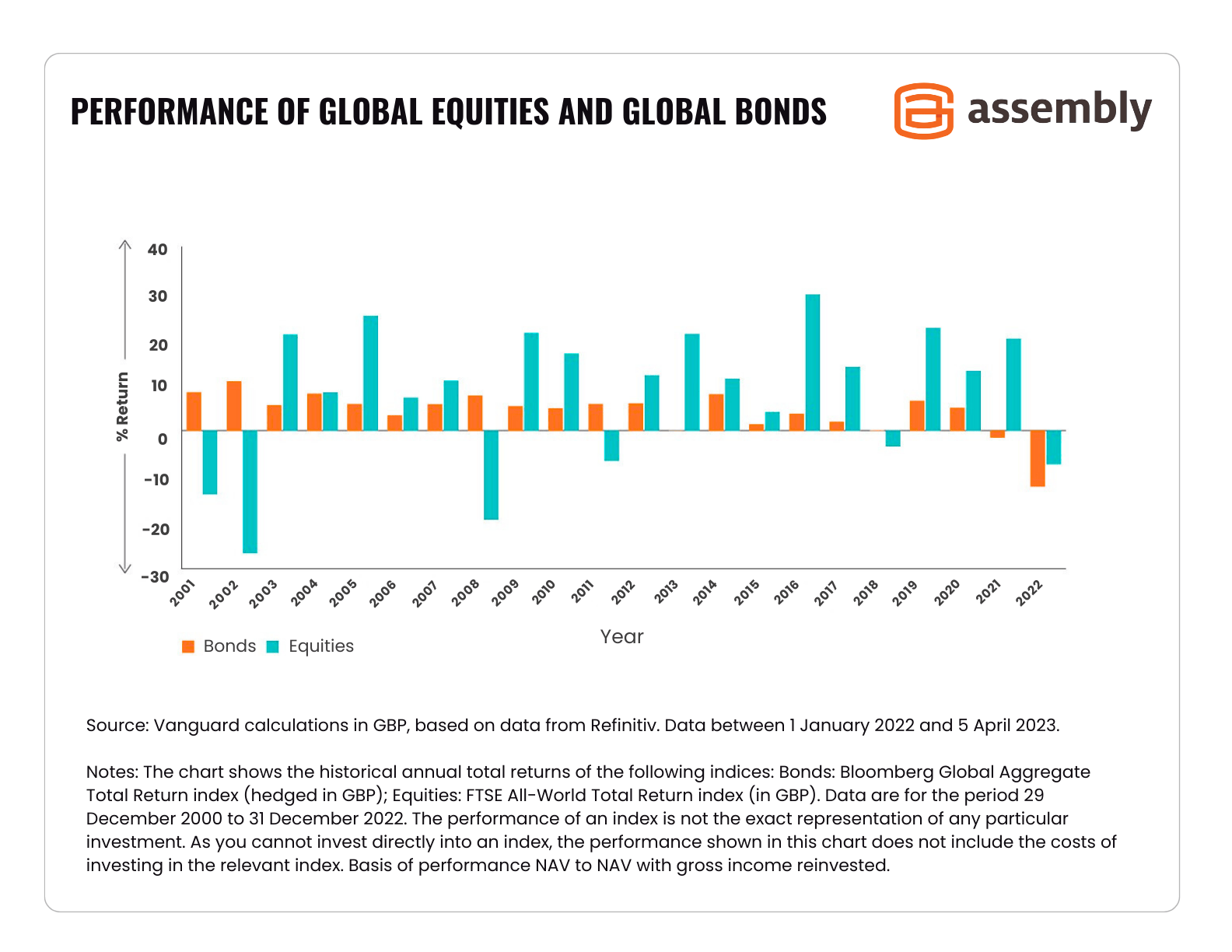

2022: A Unique Challenge for Diversification

In 2022, a combination of high inflation, rising interest rates and geopolitical tensions caused both equity and bond markets to decline sharply. This rare event led some to question the viability of diversification, yet it was the only year since 2000 in which both asset classes posted negative returns. One year’s performance does not speak for the strength of a strategy.

Historically, diversification has helped investors with both returns and peace of mind. Its performance in 2022 should be viewed in context.

Investors typically have a range of different accounts; 401(k)s, Roths and individual accounts all have different tax structures. While you could dedicate a portion of each account to equities and a portion to bonds, there are ways to potentially enhance tax efficiency by allocating accounts in certain ways.

For instance, it may be beneficial to hold stocks in taxable accounts because stocks that have declined in value can be used to offset gains through tax loss harvesting. Meanwhile, bonds, which typically generate income, can be held in tax-advantaged accounts like IRAs or 401(k)s. This strategy allows for tax-deferred growth or even tax-free growth in the case of a Roth IRA, optimizing the portfolio's overall tax efficiency. A financial advisor can help you choose tax-advantaged allocations.

Typically, during market downturns, one of the two asset classes (stocks or bonds) provides some level of positive return, helping to buffer the overall portfolio. Investors who panic and attempt to time the market may end up missing out on the long-term benefits of a diversified strategy. The key is maintaining a long-term perspective and rebalancing periodically to ensure the portfolio remains aligned with financial goals.

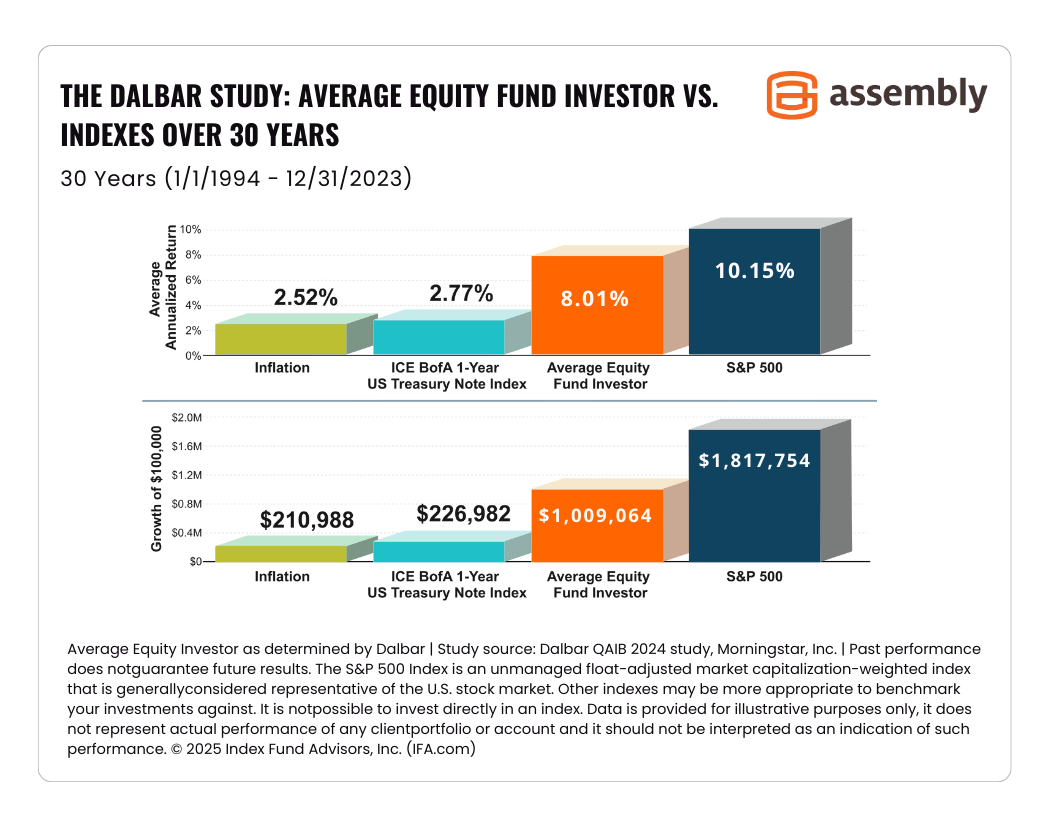

As evidenced by the gray versus the orange boxes in Dalbar’s 2024 Quantitative Analysis of Investor Behavior, the average equity fund investor often underperforms the broader market in part by trying to time entry and exit points. A disciplined, long-term approach with a diversified portfolio remains an effective way to navigate market fluctuations.

Dalbar’s 2024 Quantitative Analysis of Investor Behavior...

Diversification remains one of the most reliable strategies for managing risk and achieving consistent investment performance over time. While market conditions change, the fundamental benefits of spreading investments across asset classes remain constant. Whether through a balanced portfolio like a 60/40 allocation or more complex multi-asset approaches, diversification helps investors navigate uncertainty and stay on track toward their financial objectives.

If you're unsure how to build a diversified portfolio that aligns with your goals, consider speaking with an experienced financial advisor. A well-planned investment strategy can provide peace of mind and set you up for long-term success.

Questions? We’re here to help. Let us know what goals you’d like to achieve and what challenges you face. Connect with us online or give us a call at (415) 541-7774.

Related Reading:

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

With the year coming to a close, now is a good time to do an annual review of your financial health. Here are 10 financial planning items to review...

When the Fed reduces its federal funds rate, it creates both challenges and opportunities for investors. If you’ve been waiting to buy a car or home,...

It may look like a typo, but dollar-cost ravaging is a real thing — and a serious problem for some retirees. As you may have guessed, the name is a...