Doug Hutchinson

Doug Hutchinson

When to Take Social Security: 5 Key Considerations

Choosing when to file for Social Security benefits is one of the biggest decisions you’ll make leading up to retirement. The timing can significantly...

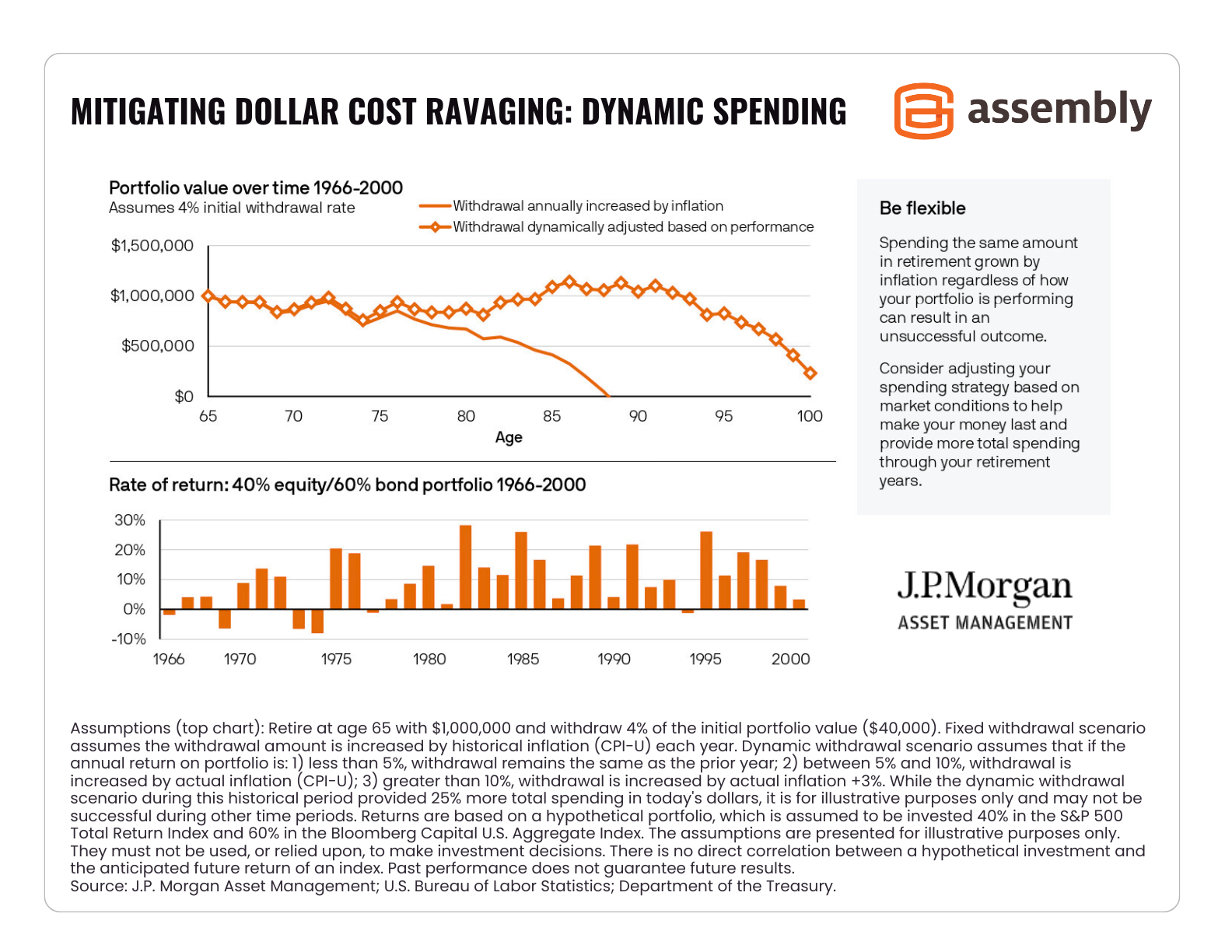

It may look like a typo, but dollar-cost ravaging is a real thing — and a serious problem for some retirees. As you may have guessed, the name is a takeoff on dollar-cost averaging, an investing strategy that involves buying a security on a regular basis regardless of share price.

Dollar-cost ravaging describes what can happen to a portfolio when withdrawals are made without accounting for market highs and lows. Retirees who follow the 4% rule are especially susceptible to dollar-cost ravaging.

Here’s what you need to know:

Investing a fixed amount on a regular basis is one of the best ways to build a retirement nest egg. Dollar-cost averaging is a popular savings strategy because it takes the emotion out of investing. You simply invest the same amount regardless of whether the market is up or down and your savings compounds over time.

Unfortunately, this strategy doesn’t work in reverse. Withdrawing a fixed amount regardless of market conditions can have the opposite effect, “dollar-cost ravaging” your portfolio balance. During a down market, more securities must be sold to maintain a set income level. With fewer assets to compound or pay dividends, the portfolio can fall into a downward spiral, especially if the down market occurs early on in the investor’s retirement

The 4% rule is a drawdown strategy that made sense when life expectancies were shorter. It’s straightforward and easy to execute:

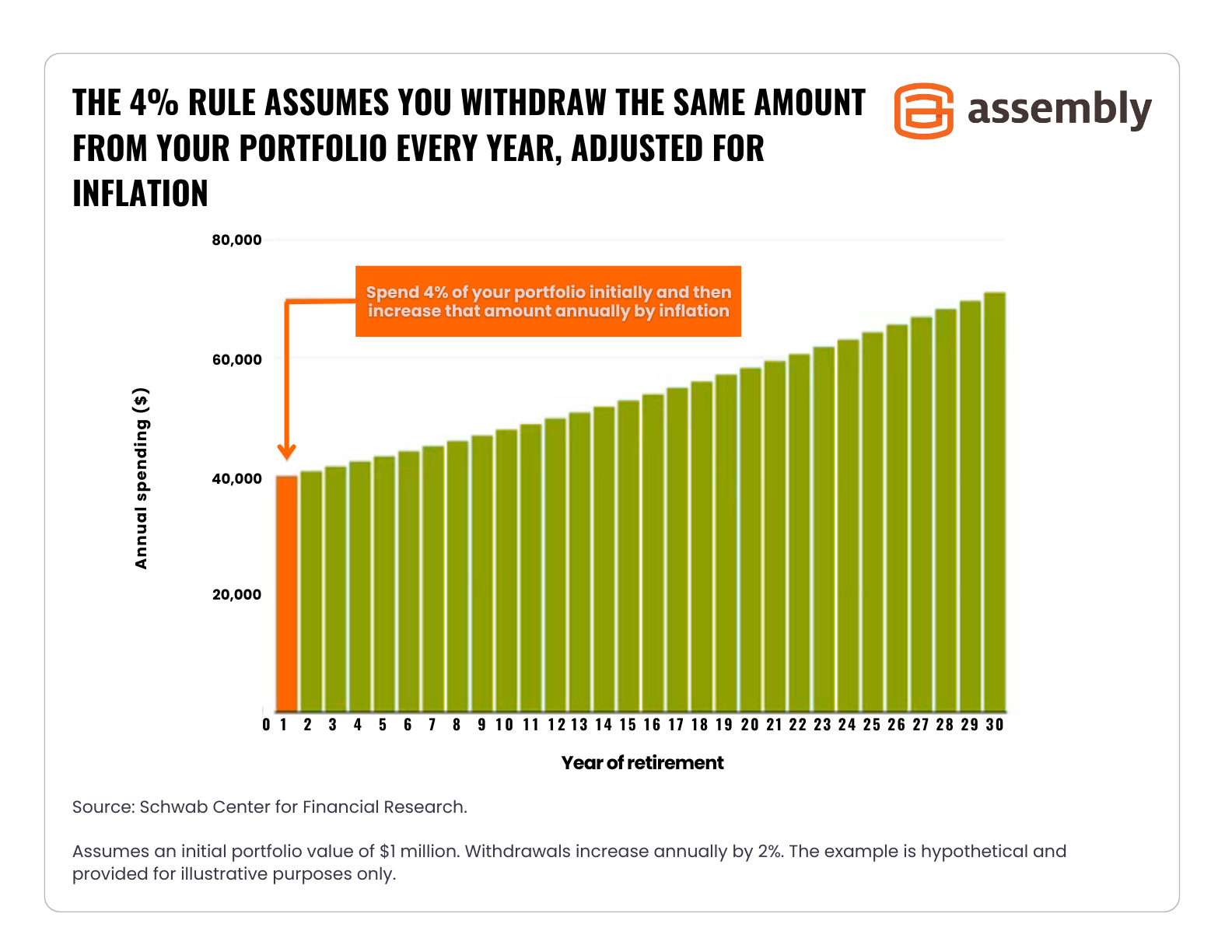

The chart below shows the 4% rule in action. The example retiree has a portfolio valued at one million dollars when they retire.

If the retiree lives for more than 30 years or if there’s a bear market early on, this person could outlive their savings. That’s why the 4% rule should be just a starting point, not an unbreakable rule.

Instead of asking, “how much return can I expect?” switch your focus to, “which investments will generate reliable income?” The income could come from dividend-paying stocks, annuities or other fixed-income investments.

It is crucial to ensure that your portfolio is properly diversified between US stocks, bonds, and non-US stocks. A well-diversified portfolio is the best way to reduce risk in the event of a potential market correction while still potentially maintaining upside for the future. A financial advisor can help you create a portfolio designed to withstand the ebbs and flows of the market.

If you're already retired, a dynamic approach can significantly extend the life of your retirement savings. Instead of withdrawing a pre-determined amount every year, calculate how much (or how little) you can withdraw depending on whether the market is up or down.

Your withdrawal strategy is just as important as your savings strategy. We can help you craft a wealth of life plan customized to your needs and goals. Contact us online or give us a call at (415) 541-7774.

Related Reading:

Disclaimer: Assembly Wealth is neither an attorney nor accountant, and no portion of this content should be interpreted as legal, accounting or tax advice. Individuals should consult with an investment professional, or an attorney or tax professional regarding their specific investment, legal or tax situation.

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

Choosing when to file for Social Security benefits is one of the biggest decisions you’ll make leading up to retirement. The timing can significantly...

When the Fed reduces its federal funds rate, it creates both challenges and opportunities for investors. If you’ve been waiting to buy a car or home,...

If you have a taxable investment account, tax loss harvesting could help you reduce your tax burden. Before the year is out, take a look at your...