Doug Hutchinson

Doug Hutchinson

How to Invest When the Market is High

With US equity markets trading near all-time highs1, some investors may be concerned about a sell-off in the near future. While this thinking may...

When the Fed reduces its federal funds rate, it creates both challenges and opportunities for investors. If you’ve been waiting to buy a car or home, lower interest rates are beneficial. Unfortunately, it also reduces returns on savings accounts, certificates of deposits (CDs) and money market funds.

Those who have enjoyed close to a 5% annualized yield may want to move their money out of savings, CDs and money market funds into investments with higher returns.

Here are some strategies to consider:

The federal funds rate is the interest rate at which banks can lend money to one another overnight to meet reserve requirements. The Federal Reserve (“the Fed”) can periodically raise or lower this rate to create monetary policy. While this economic lever seems far removed from our everyday life, small changes can have a big impact on our economy, affecting interest rates on mortgages, car loans, credit cards or savings accounts.

When the Fed lowers the federal funds rate, money is “cheaper” to borrow. It encourages individuals and businesses to take loans, spend and invest. Increased borrowing and spending stimulates the economy, making rate cuts an effective strategy to steer the economy away from a recession or out of an economic turndown.

Conversely, when inflation is high, the Fed raises its funds rate. Money becomes more expensive and economic activity slows.

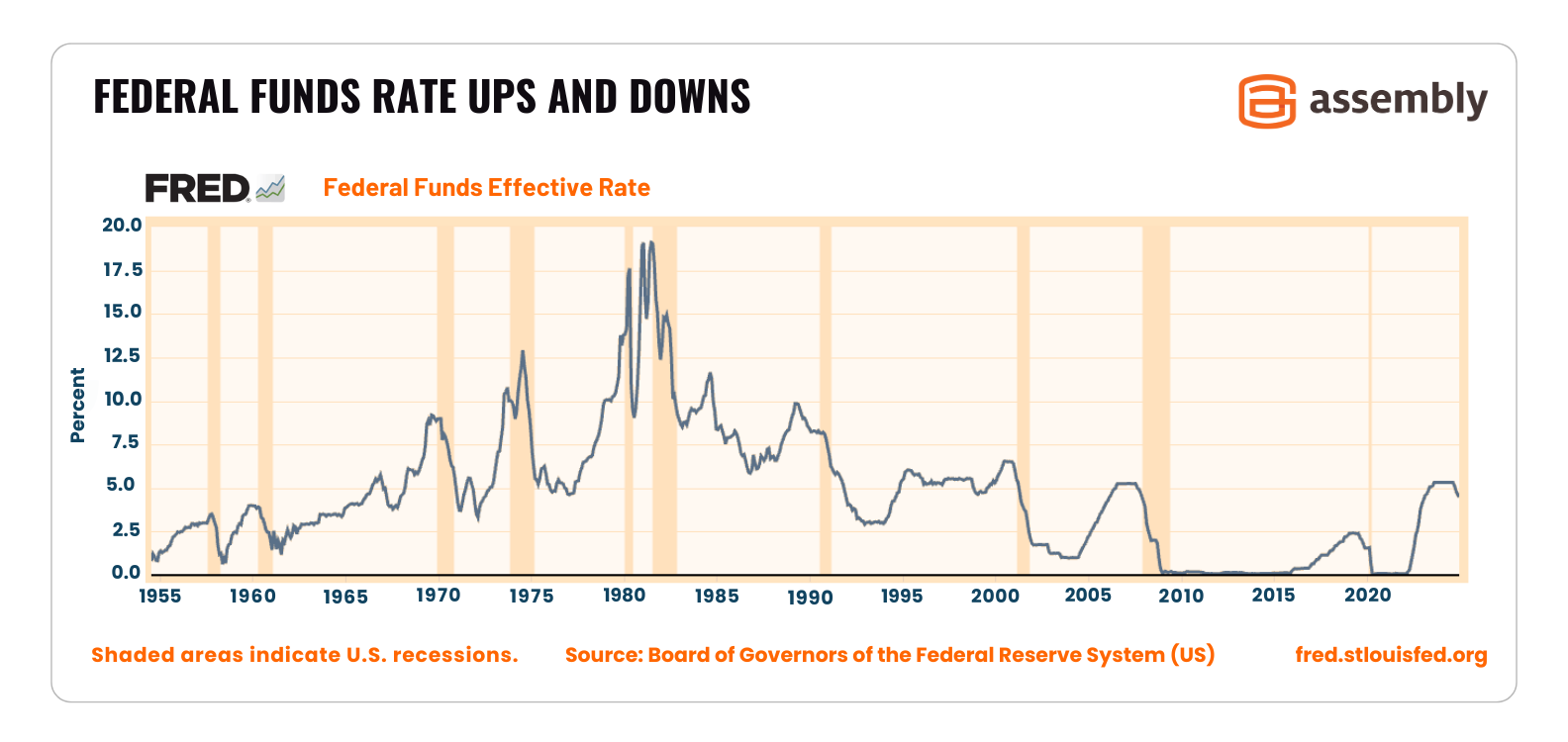

Federal Funds Rate Ups and Downs

As seen in the graph below, the federal funds rate has fluctuated dramatically over the decades in response to inflation and recessions. In the 1980s, it peaked near 20%, to combat double-digit inflation rates. This is a stark contrast to the late 2000s, when rates were near zero to fight the Great Recession.

A Soft Landing

Rates were lowered at the start of the pandemic to encourage spending, then raised as life came back to normal and inflation started to rear its head. As inflation gets under control, rates are being cut again.

Federal Reserve Chair Jerome Powell has been navigating rate adjustments in order to achieve a “soft landing” for the economy. The goal is to rein in inflation to 2% while not triggering a recession.

Market sentiment is that we are in for a soft landing, but we will have to follow along and see as the Fed continues to cut rates into 2025. By staying informed and proactive with your investments, you can be positioned to gain from falling rates while staying diversified.

We never recommend trying to time the market, but certain sectors can potentially benefit from rate cuts. These sectors include capital-intensive industries and financial industries such as:

Cheaper borrowing costs allow companies to expand and invest in research and development. Small-cap stocks, which often rely on borrowing to grow, also tend to thrive in low interest rate conditions. Consumer discretionary stocks may also get a boost because lower borrowing costs give households more disposable income to purchase non-essential goods and services.

For income-seeking investors, dividend stocks can provide a steady cash flow. When combined with price appreciation, the total value could match or beat the income received from 5% yields on money market funds and CDs. Companies that issue dividends are typically utilities, communications and consumer staples — sectors that can remain fairly stable in times of economic uncertainty.

Bond yields typically decline as interest rates fall, but that doesn’t mean they aren’t a good place to invest. Locking in bonds with higher rates before further cuts can offer both income and price appreciation because higher rates are more attractive to investors.

High-yield bonds can offer higher returns to compensate for their increased risk. While they can be a valuable part of a diversified portfolio, balancing this risk with other safe investments is essential. Speak with a financial advisor to determine the appropriate allocation for your situation.

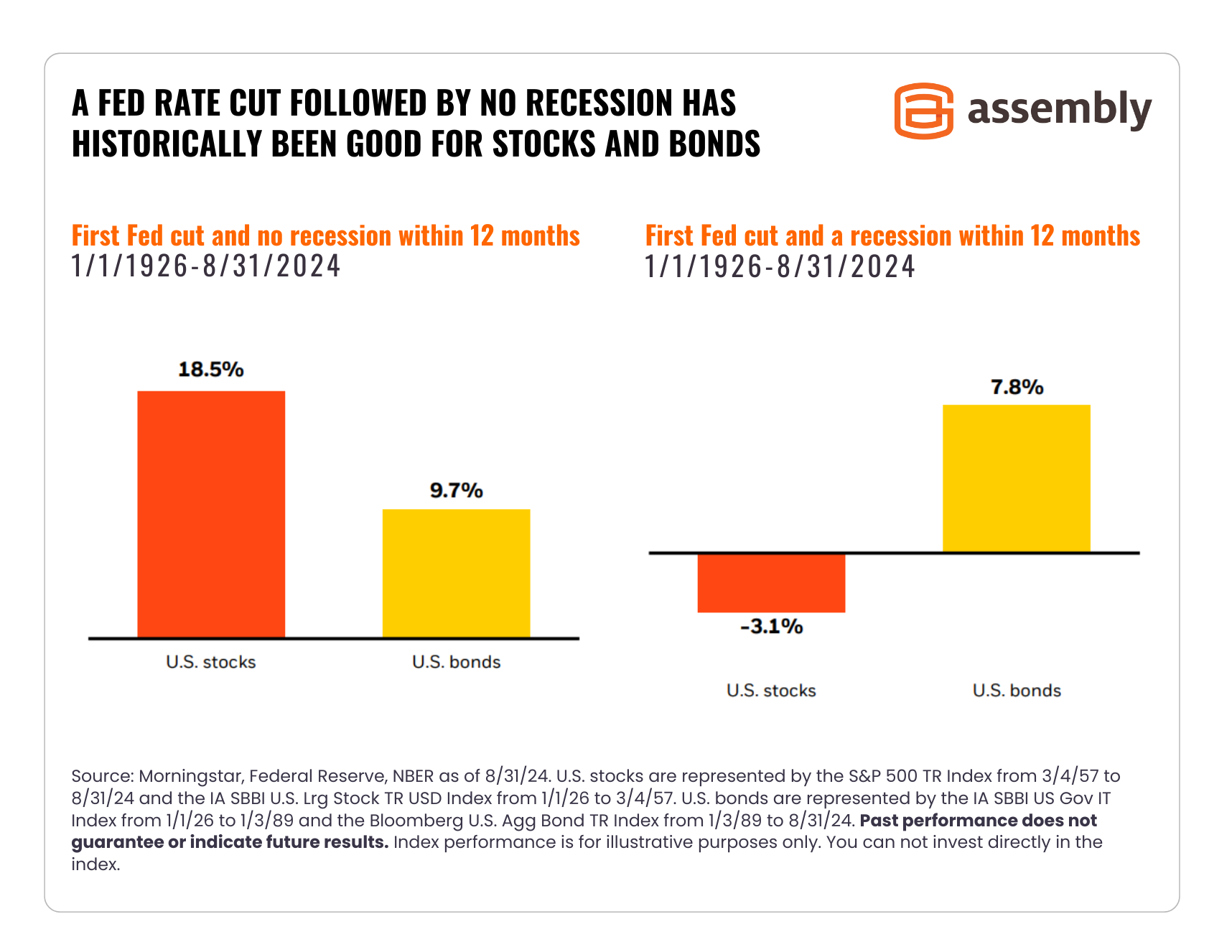

On average, U.S. stocks have surged 18.5% in the year following the Fed’s first rate cut if no recession occurs. During the same period, bonds have returned 9.7%.

In cases where a recession follows the rate cut, stock returns have averaged a decline of 3.1%, with bonds returning slightly less than in non-recession years. These historical trends underscore the importance of diversification and a balanced approach to investing during times of rate changes.

Real Estate

As mortgage rates drop, property can become more affordable. This may drive up demand and potentially lead to increased property values.

Real estate investment trusts (REITs) offer exposure to the real estate market without having to buy an actual property. These funds often pay dividends as well.

Cash

While interest rates were high, many investors kept a large chunk of cash in money market funds. However, as rates decrease, investors may want to reallocate their money into investments offering a higher return.

Cash is still an important part of a portfolio, however. It can keep your allocation set up correctly, and it’s wise to have an emergency fund with at least 6-9 months of living expenses in cash. If the need arises, you’ll have liquid funds to fall back on.

Now is an excellent time to revisit your financial plan, or get one started if you don’t have one. Speak to a financial advisor about strategies tailored to your goals, risk level and time horizon.

If you’re unsure how the Fed’s rate changes will impact your current investments, please reach out. An advisor can help you create a plan that benefits from declining rates while helping you achieve your long-term goals.

Related Reading:

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios. Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

With US equity markets trading near all-time highs1, some investors may be concerned about a sell-off in the near future. While this thinking may...

Diversification is one of the most effective strategies for managing risk and improving long-term investment outcomes. By choosing investments across...

In June 2024, Nvidia (NVDA) became the largest publicly traded company in the world for the first time, briefly surpassing Microsoft. Throughout...