Through the end of 2025, only estates worth more than $13.61 million are subject to federal estate tax. Under the current law, only a tiny percentage of estates are taxable at the federal level .

The estate tax exemption threshold is scheduled to drop to $7 million per individual or $14 million for a married couple (estimated) starting in 2026. Congress and the President will determine if the higher estate threshold will be extended or allowed to sunset by the end of 2025. We’ll share the news with our email subscribers and followers on Facebook, Instagram and LinkedIn if and when any changes are signed into law.

If your estate is under the current (or projected) federal estate tax exemption, here are some tax optimization strategies we recommend:

Disclaimer: Assembly is neither an attorney nor accountant, and no portion of this content should be interpreted as legal, accounting or tax advice. Individuals should consult with an investment professional, attorney or tax professional regarding their specific investment, legal or tax situation.

There’s a significant tax advantage to transferring appreciated assets through an estate or trust instead of a gift. Inherited assets are valued using a stepped-up basis, which can help beneficiaries significantly reduce the amount of capital gains tax owed on an asset that may have been purchased before they were born.

A stepped-up basis means the “cost” of an inherited asset is the fair market value at the original owner’s time of death, not the original cost. Put another way, if the deceased person owned an appreciated asset (securities, a home, etc.), beneficiaries don’t have to pay capital gains on the appreciation that occurred while the deceased person was alive if the asset is transferred upon death.

Example:

A grandmother purchased 100 shares of a $10 stock in the 1990s. The stock is now worth $1000 per share. If Nana sells the stock, she’ll pay capital gains on the $900 appreciation for every share she sells. Similarly, if she transfers ownership to her favorite grandchild while still alive, the grandchild will have the same capital gains liability.

If grandma leaves the stock to her favorite grandchild in her estate, the cost basis becomes $1000 (or whatever the fair market value is on the date of her death). Down the road, if the grandchild sells the shares for $1200 per share, they’ll only pay capital gains on $200 per share (the difference between the stock’s value on the day they acquired it and the sale price).

A stepped-up basis cuts both ways. For appreciated assets, there’s a huge tax benefit. But if the house, stock or other asset loses value, the heir cannot take a tax deduction.

Consult a financial advisor if you’re unsure whether to keep an asset in your estate versus selling it, transferring it or including it in a trust.

Retirement accounts, such as IRAs and 401(k)s are not eligible for the step-up basis. Assets held in non-taxable accounts are subject to applicable state and federal taxes when funds are withdrawn.

Non-spousal beneficiaries have a maximum of 10 years to withdraw the funds in an inherited IRA, and spouses must begin required minimum distributions (RMDs) within one year of the decedent's death. If the deceased’s heirs are close to or in the top tax bracket, Uncle Sam can take up to 37% of the inherited funds since these distributions are taxed as ordinary income.

Below are a few ways to minimize the tax liability on an inherited IRA. Please keep in mind each strategy is situation-dependent. The best option will depend on the beneficiary’s age, expected income and long-term goals. An experienced wealth manager can help you create a personalized plan.

Calculated withdrawals: Carefully timed distributions can help beneficiaries avoid moving into a higher tax bracket.

Tax loss harvesting: If a beneficiary owns securities with unrealized losses in a non-retirement account, the underperforming assets can be sold and the capital loss can be used to offset some of the RMD income. Up to $3000 may be deducted from ordinary income per year and the remainder can be deducted in future years. Learn more about tax loss harvesting.

Split IRA: In families where there are two spouses and at least one descendent, it may be beneficial to split the deceased IRA between the spouse and descendent(s). This gives the descendent(s) 10 years to draw down the first part of the IRA. When the second spouse dies, the descendent(s) get a new 10-year period to withdraw whatever remains.

Qualified charitable distributions (QCDs): If the beneficiary is over 70½, they can make payments directly from a traditional IRA to a qualified charity. Up to $105,000 per year can be distributed tax-free for 2024. Learn more about the pros and cons of QCDs.

Roth Conversions: Roth IRAs are still subject to the 10-year rule, but withdrawals are not taxable. It may make sense to gradually convert a traditional IRA to a Roth IRA for the purposes of inheritance.

If the original owner is in a lower tax bracket than the beneficiary, moving money out of a traditional IRA to a Roth (gradually or all at once) will allow the beneficiary to inherit tax-free money. Consult a financial advisor or tax professional to avoid converting too much at once and ending up in a higher tax bracket.

If the recipient is in a lower tax bracket than the IRA owner (and expects to remain there), keeping the traditional IRA may be the more tax-efficient strategy. When the original owner passes, the beneficiary can choose to convert the IRA to a Roth IRA in anticipation of future tax savings or simply draw the account down over 10 years.

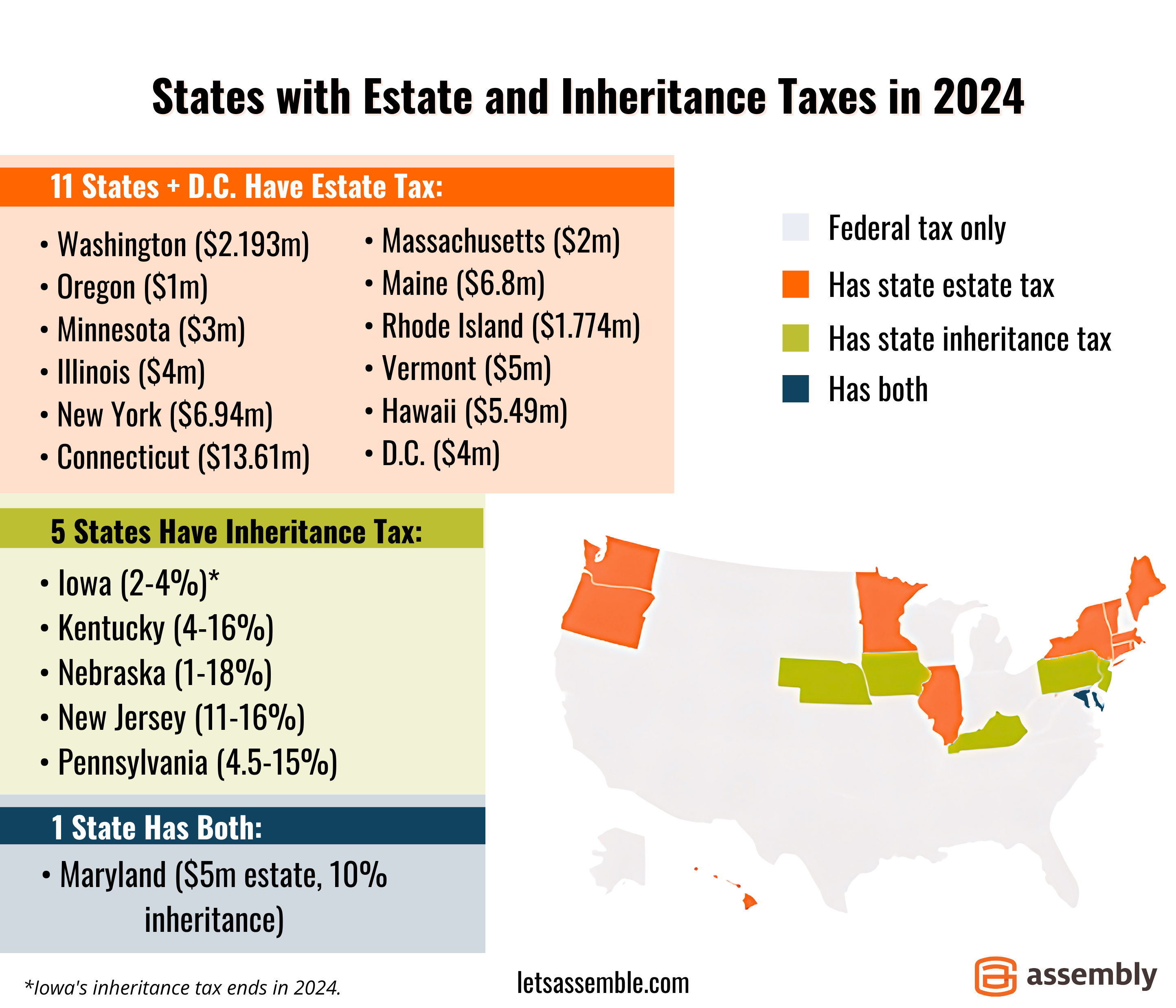

As of writing, 17 states have either an estate or inheritance tax. Twelve states and Washington D.C. have thresholds below the federal tax exemption level. In other words, estates that are non-taxable at the federal level may still be taxable at the state level.

Additionally, some states don’t allow deduction portability — a provision in which the surviving spouse “inherits” the unused portion of their deceased spouse's tax exemption. Portability can only be applied in the tax year someone passes away, but it can make a significant difference in taxable income.

In some states, inheritance and estate taxes apply to non-residents. For example, the descendants of someone with assets located or registered in Oregon (such as a home, boat or plane) may have to pay Oregon estate tax on those assets, even if no one in the family is (or was) an Oregon resident. At the very least, an Oregon state tax return must be filed.

Inheritance tax is based on the value of the assets each beneficiary receives and their relationship to the deceased. Surviving spouses are exempt from inheritance tax and, in some states, children and grandchildren are too. In states where children, grandchildren and close family members are taxed, it’s usually at a lower rate than assets gifted to non-family members.

A financial advisor can help you maximize your gift to loved ones or charitable organizations. Schedule a free consultation to find out if your estate plan is:

Related Reading:

{kind=link}