Doug Hutchinson

Doug Hutchinson

Year-End Financial Planning Checklist

With the year coming to a close, now is a good time to do an annual review of your financial health. Here are 10 financial planning items to review...

Saving for retirement can feel like an uphill battle, even for couples. Planning for retirement solo can feel both liberating and daunting. You get to call the shots, but you also have to cover all the expenses — including the unexpected ones.

Whether you’re single by choice or circumstance, you don’t have to go it alone. A financial planner can help you glide into your golden years with confidence and freedom — but you have to start sooner rather than later. In this article, we'll share surprising statistics and practical strategies for single retirees.

The image of a cozy retirement often features couples strolling hand-in-hand, but what about the millions of people who are happily (or unexpectedly) flying solo? According to recent government data, 29% of U.S. households have only one person. Roughly 38 million Americans live alone, a fivefold increase since 1960.

Unfortunately, 42-50% of older people living alone don’t have enough income to meet their basic needs (as defined by the Elder Index). There are many reasons to start saving for retirement early, but building a strong financial foundation is critical for people who may spend their golden years solo.

A common question we help people answer is, “Am I saving enough for retirement?” The honest answer is: the amount of money you need to save depends on your goals.

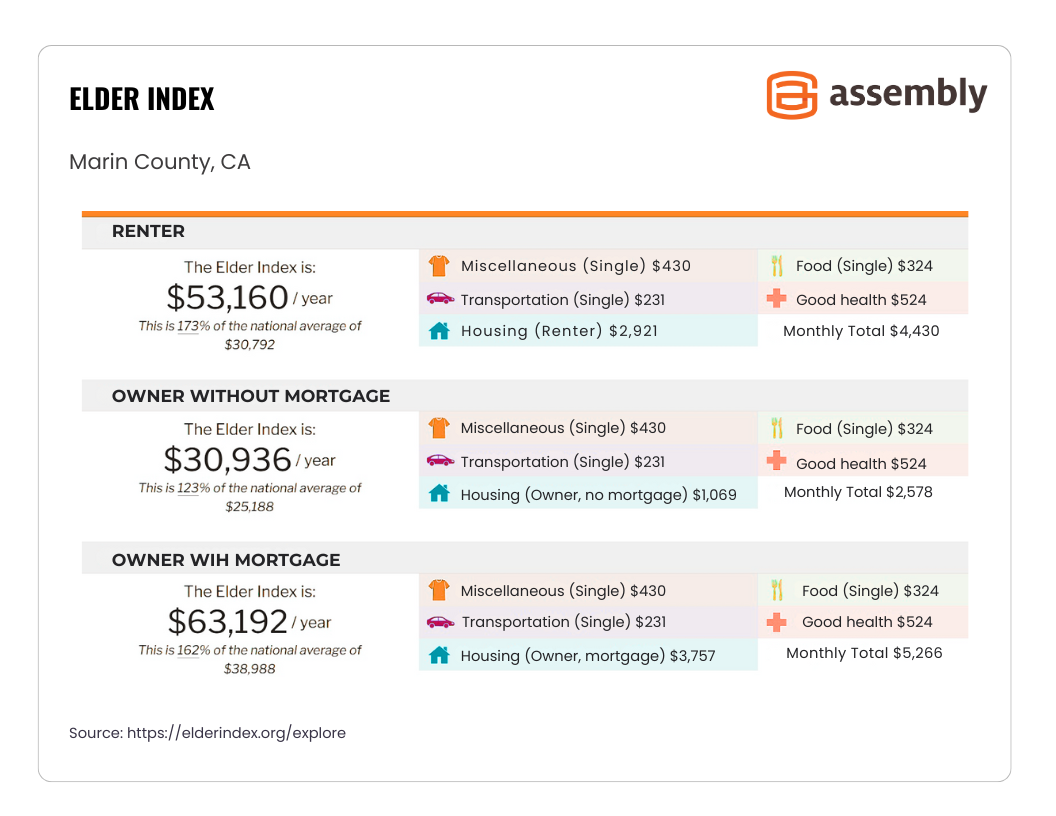

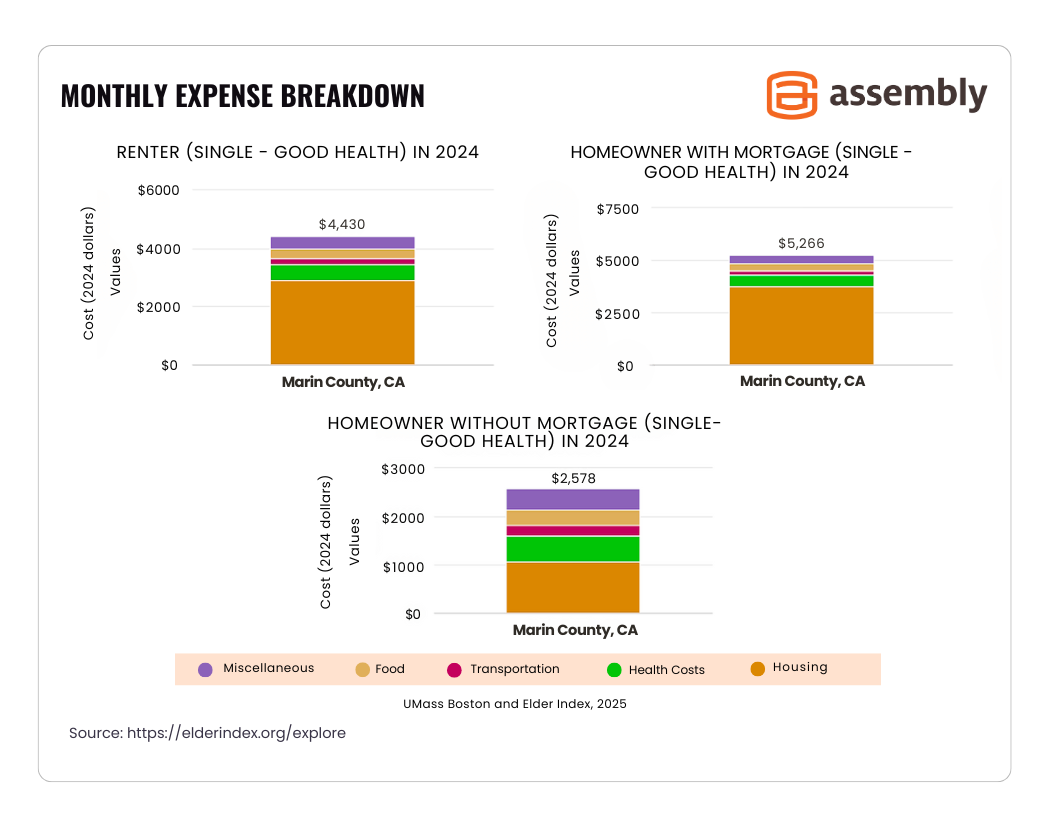

As a baseline, you can use The Elder Index to find out how much it costs to pay for basic needs in a particular area. The graphs below show estimates for Marin County, where our office is located. You can check the Elder Index for your county and most major metropolitan areas in the U.S. and adjust the figures based on your expected health status and whether you expect to be paying a mortgage.

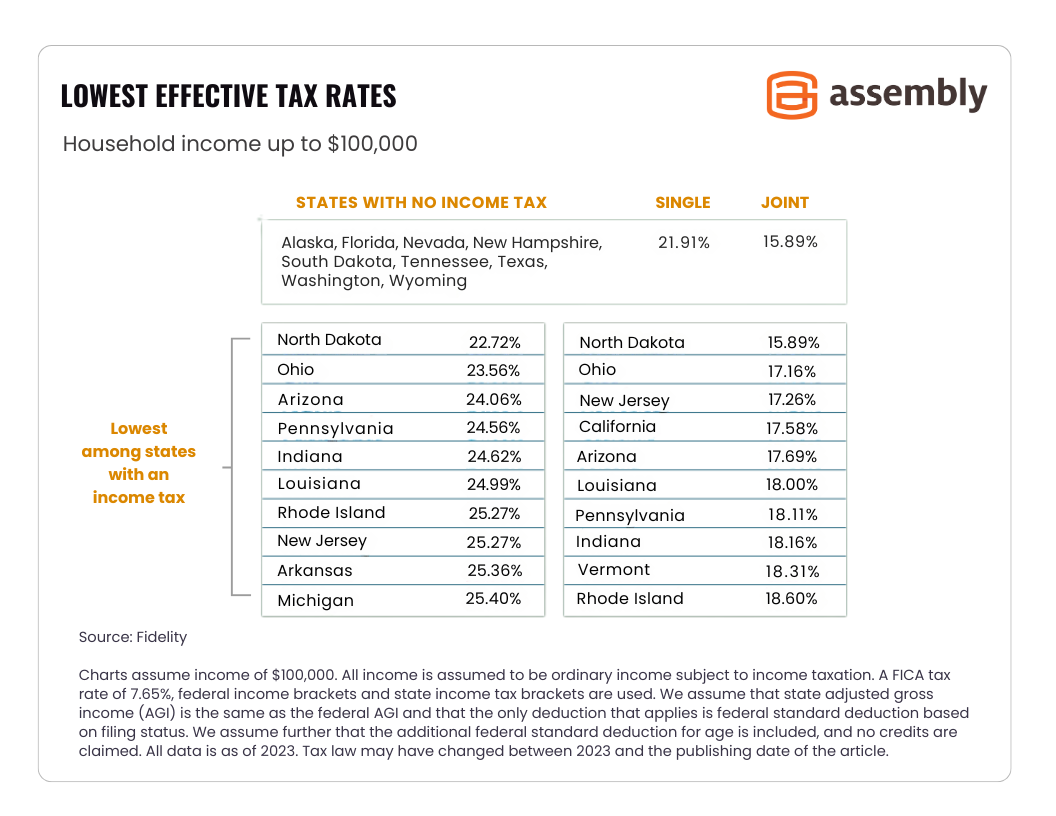

Living without a partner typically means your living costs are higher — now and in the future. That’s why tax-efficient investing is so important.

Giving less money to the taxman allows you to invest in Future You. A financial planner can help you identify the best approach, but here are a few ways you can reduce your tax burden:

Single parents should consider a 529 account for educational expenses. Contributions are not tax deductible at the Federal level, but your money grows tax-free and withdrawals are tax-exempt when used for qualified educational expenses. Qualified expenses include: tuition, fees, textbooks and housing.

Experts recommend having sufficient cash or liquid assets to cover three to six months of living expenses. Single people, especially single parents, should consider having at least six to nine months of living expenses to overcome unexpected financial challenges. The last thing you want to do is dip into your retirement savings to cover an emergency home repair or medical bills. Learn more about The Toxic Effects of 401(k) Loans and Early Withdrawals.

Some employers offer short and long-term disability insurance. If you’re self-employed or don’t have access to this type of coverage, you can purchase policies that help cover treatment and rehabilitation costs following an accident, cancer diagnosis or other critical illness.

Some people joke about leaving everything to a beloved pet, but who will take care of your furry friend when you’re gone? What happens to Felix or Fido if you end up in a rehab center or long-term care facility that doesn’t allow animals?

Retirement planning for singles includes end-of-life planning as well. Here are a few considerations for people who expect to spend their retirement without a (human) partner:

A Power of Attorney (POA) — Someone legally empowered to make medical decisions and handle financial matters. This can be the same person, or two different people. Learn more about creating a Power of Attorney.

Long-Term Care Insurance (LTC) — In their final years, many people can no longer live independently. The cost for LTC coverage increases as you age and may not be available to people 70 or older, so it’s worth looking into.

An Advance Medical Directive — Both single people and those in a committed relationship should have an advance medical directive, a written statement telling doctors and loved ones what to do (or not do) if you cannot communicate. The National Institute on Aging has forms and helpful information.

We’ve written a lot about estate planning and how to avoid common mistakes. The biggest issue for both single retirees and married people is not having a plan in place.

Don’t wait until an accident or medical diagnosis forces you to make important decisions when you’re in crisis mode. Instead, set aside time to consider what you’d like your legacy to be. Is there a charitable organization you’d like to support? Friends who need help paying for college? A financial planner can offer ideas, act as a sounding board, and ultimately help build out an estate plan that can include charitable giving and an inheritance to family or friends while optimizing tax efficiency.

For people who are single because of a separation or divorce, the biggest estate planning mistake is not updating their beneficiaries. There are many sad stories of ex-partners who (legally) got everything and refused to share the inheritance. .

Whether you've chosen to go it alone or simply haven't found the right partner, you deserve to have a comfortable retirement. It starts with a tailored strategy that:

Our experienced wealth managers can help you design a personalized retirement savings strategy you’ll feel confident about. Start your Wealth of Life Plan by contacting us online or by phone (415) 541-7774.

Related Reading:

Disclaimer: Assembly Wealth is neither an attorney nor accountant, and no portion of this content should be interpreted as legal, accounting or tax advice. Individuals should consult with an investment professional, or an attorney or tax professional regarding their specific investment, legal or tax situation.

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

With the year coming to a close, now is a good time to do an annual review of your financial health. Here are 10 financial planning items to review...

If you have a parent age 65 or older and at least one dependent child, you’re a member of the sandwich generation. According to Pew Research, about...

To ensure your assets are distributed in accordance with your wishes, detailed financial planning is essential. Without a legal will, up-to-date...