Doug Hutchinson

Doug Hutchinson

How To Protect Your Financial Information Online

You’ve worked hard to save and plan for a healthy financial future. Unfortunately, cybercriminals are also hard at work — devising ways to steal your...

Choosing when to file for Social Security benefits is one of the biggest decisions you’ll make leading up to retirement. The timing can significantly impact how much money you’ll receive over your lifetime.

You can start collecting Social Security at age 62, but waiting until your full retirement age — or even later — can mean a substantially higher monthly benefit. Delaying benefits can be a hedge against longevity, but it’s not the best strategy for everyone.

The charts below can help inform your decision, but we’re always here to help. Please don’t hesitate to contact us with any questions you may have.

Even people who have saved and invested carefully worry about outliving their savings. Waiting to collect Social Security can provide more financial security throughout retirement, but delaying Social Security payments may mean withdrawing money from your retirement account.

For some, it may make sense to collect Social Security benefits early instead of cashing out retirement investments. Reasons to delay vary, but may include a downturn in the market or a desire to let investments continue to grow.

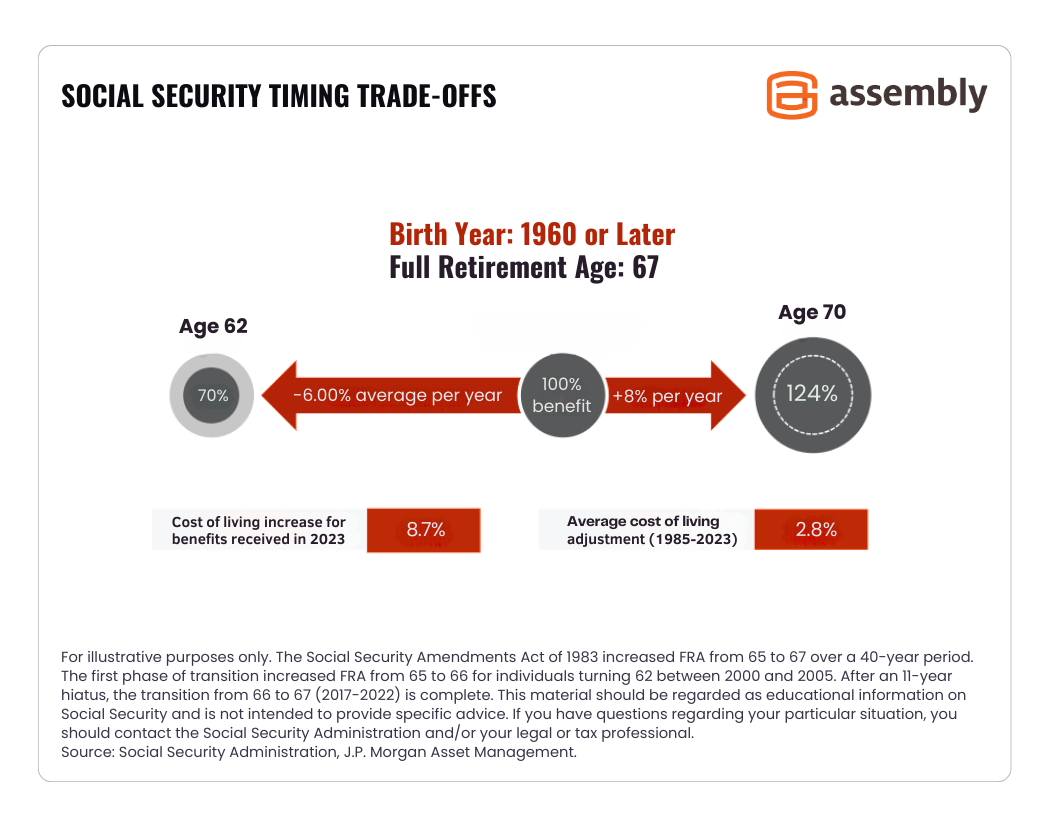

Anyone born after January 1st, 1960 can start collecting Social Security at age 62, but full retirement age is 67. Taking Social Security at age 62, 63, 64, 65 or 66 is considered “early retirement” and comes with a reduced benefit.

As the chart below shows, there’s a 6% (average) reduction for every year leading up to full retirement age. In other words:

To be clear, if you file for Social Security at age 62, you lock in the 30% reduced payment for life. It doesn’t change to a 24% reduction at age 63. You will, however, receive an annual cost of living (COLA) adjustment, which is 2.8% on average.

On the flipside, waiting to collect Social Security benefits can increase your annual payment by 8% (on average) for each year you delay. Delayed retirement credits add up until you reach age 70, at which point your benefit amount stops increasing.

Other Income

If you plan to keep working or have significant income from dividends or other sources, your benefit amount may be affected. If your earnings exceed a certain dollar amount:

When you reach full retirement age (67), you can work and earn as much as you want and your benefit will not be affected. If you’re younger than 67 and want to keep working or have substantial income from other sources, consult a financial advisor before filing for Social Security.

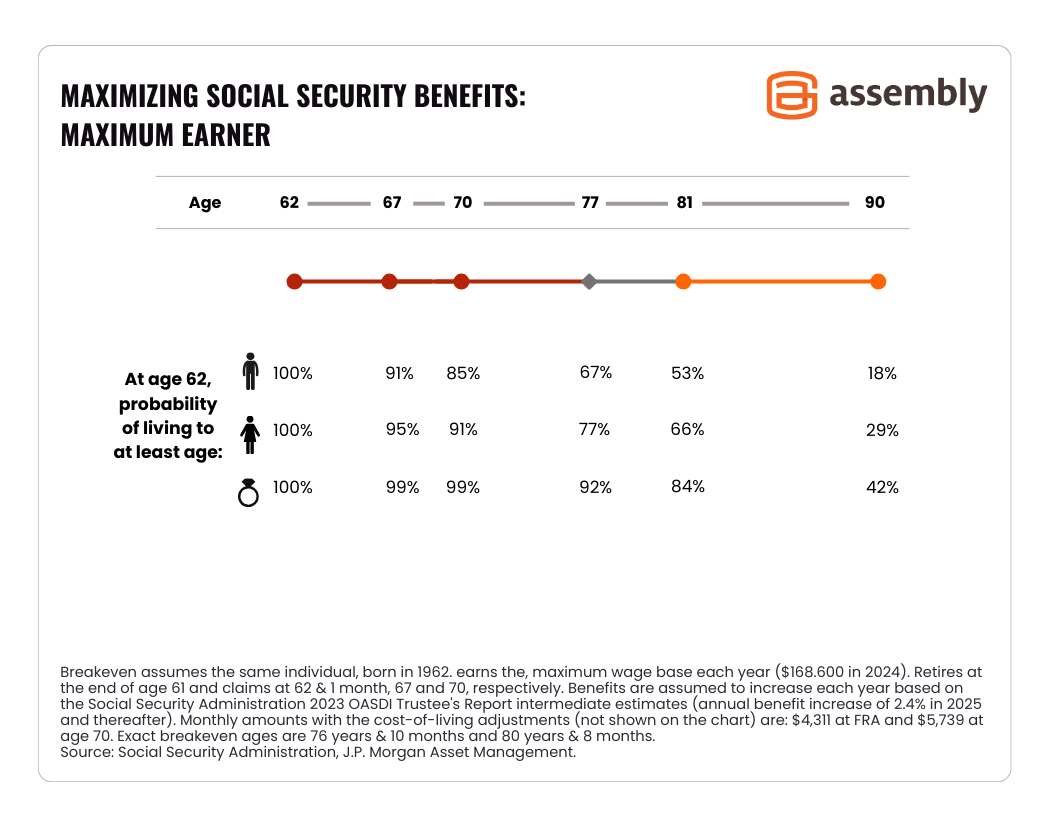

Longevity

According to the SSA (Social Security Administration), “More than one in three 65-year-olds will live to age 90.” Many factors affect longevity, including: relationship status, family history and current health.

The chart below shows the average odds of living to age 67, 70 and beyond. The ring symbol represents couples and assumes both partners live to the specified age.

If you don’t expect to live past age 77, it may make sense to start your Social Security benefits early. As the saying goes, “You can’t take it with you.” But if you expect to live beyond age 81, consider waiting until age 70 to claim your benefit.

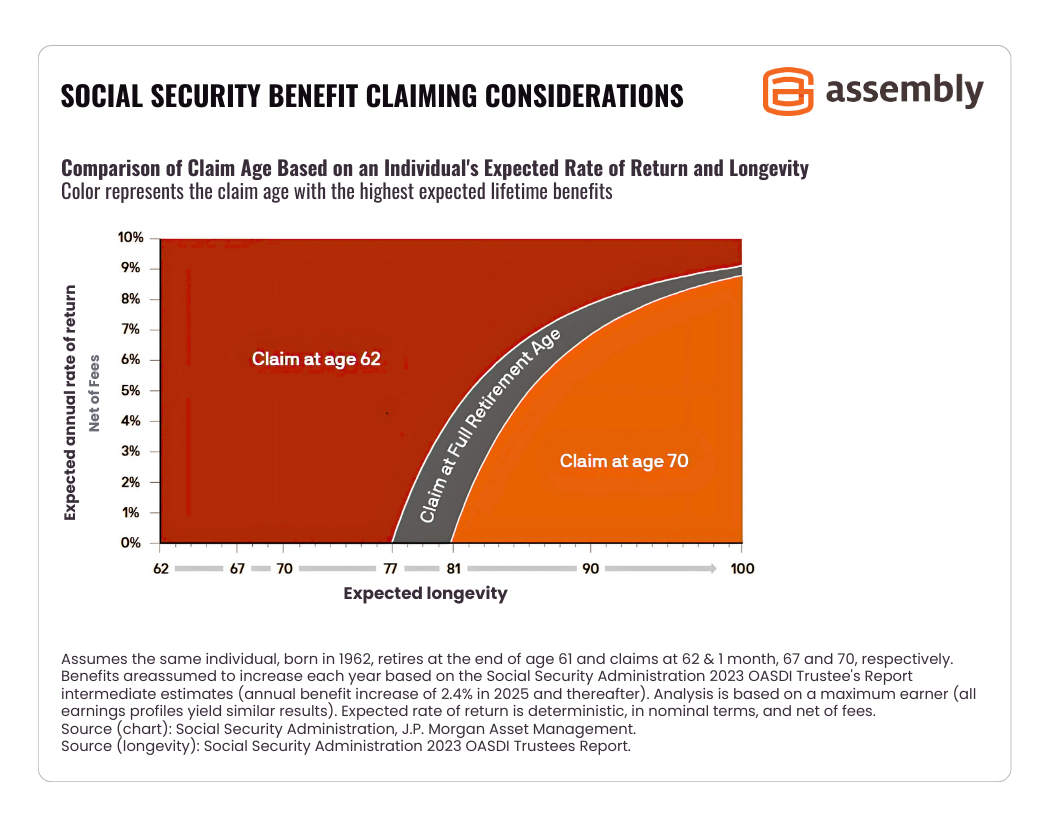

Expected Rate of Return on Savings and Investments

Your retirement savings and investments may also be a factor in when you start collecting Social Security. People who began investing for retirement later in life may want to stay invested in the stock market, while others move to fixed-income securities.

The chart below shows how varying rates of return (net of fees) factor into the best time to claim Social Security benefits. For example, someone with an expected 5.5% rate of return and a life expectancy of 88 should consider waiting until age 70 to start Social Security.

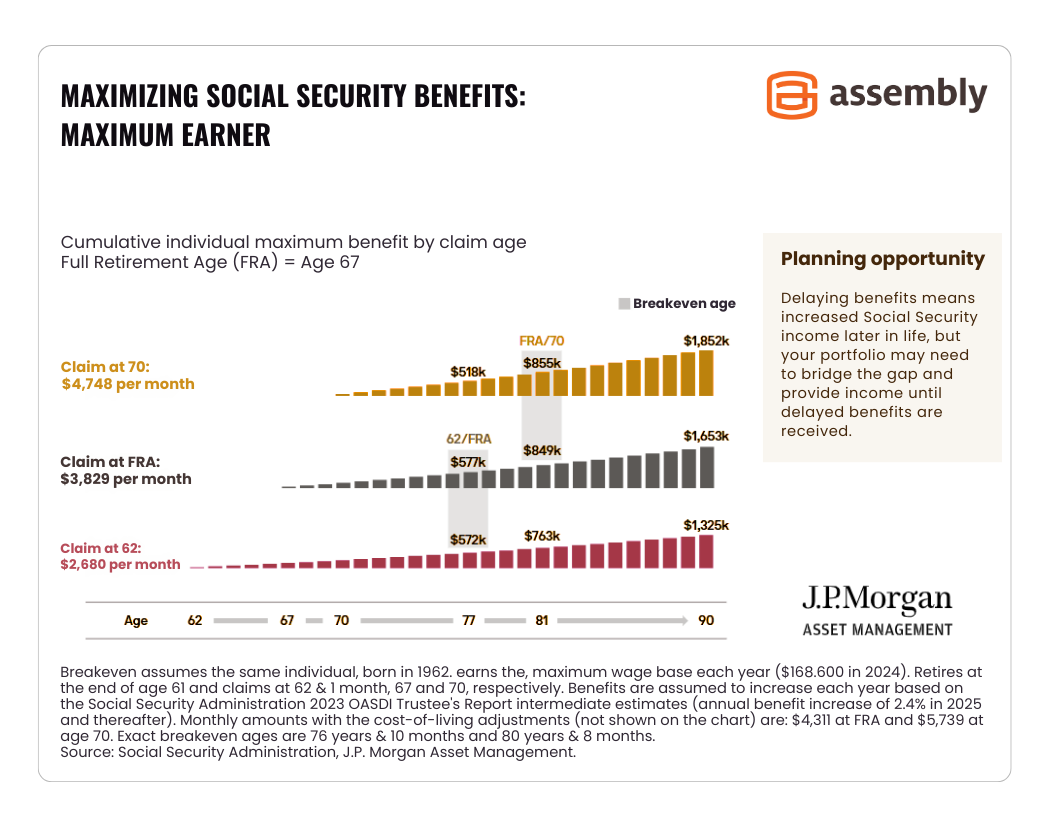

There’s a point in time where the value of waiting to start Social Security surpasses the value of collecting benefits early. This is called your Social Security “break-even” age. Calculating your Social Security break-even age can help you figure out whether it’s better to start collecting Social Security early vs waiting until full retirement age, or even age 70.

Imagine two twins, Avery and Robin. For the last 20 years, they’ve individually earned more than $176,100 per year (the maximum wage base for Social Security). Avery retires early at age 62 and receives a reduced benefit of $2680 per month. Robin keeps working until full retirement age.

At age 67, Robin starts collecting Social Security and receives $3829 per month. But at this point, Avery is way ahead — having already received more than $160,800 in Social Security payments in the past five years.

The break-even point for Avery and Robin is just before their 77th birthday. By age 77, Avery will have received $572,000 in Social Security payments, and Robin will have received $577,0000. From this point on, Robin’s lifetime Social Security payments will be higher than Avery’s.

The chart below illustrates the scenario described above. You can also compare Avery and Robin’s break-even age if one twin retired at 67 and the other waited until age 70.

Curious what your Social Security break-even age is? You can either Log in to your Social Security account to obtain your Social Security Statement and consult a financial advisor to help walk you through your benefits, retirement age scenarios, and your break-even age.

Because women typically live longer than men, waiting to claim Social Security can be a smart move. That said, this strategy may require substantial savings and/or supplemental income to cover expenses in the meantime.

For married couples, it generally makes sense for the higher earner to delay filing. This ensures the person with the highest wage base receives their maximum benefit. If the high earner dies first, the surviving spouse can choose to receive the deceased spouse’s higher benefit.

If you are divorced and at least 62 years old, you may be able to receive spousal benefits if:

It doesn’t matter if the ex-spouse has filed for Social Security, they simply need to be eligible. There are other requirements, which you can learn about on the SSA website or by consulting a financial advisor.

What retirement means to you may be quite different from what it means to someone else. We can help you make an informed decision about how and when to retire based on your specific needs and goals.

Let us know what questions or thoughts have come to mind while reading this article. Contact us online or by phone (415) 541-7774. We’re happy to help.

Related Reading:

Disclaimer: Assembly Wealth is neither an attorney nor accountant, and no portion of this content should be interpreted as legal, accounting or tax advice. Individuals should consult with an investment professional, or an attorney or tax professional regarding their specific investment, legal or tax situation.

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

You’ve worked hard to save and plan for a healthy financial future. Unfortunately, cybercriminals are also hard at work — devising ways to steal your...

When I was a kid, it annoyed me when relatives I only saw during the holidays would exclaim, “Look at how much you’ve grown!” Now that I’m an adult,...

Many Americans don’t have an estate plan because they don't like to think about a time when they will no longer be around. It's understandable, but...