Two strategies designed to maximize Social Security retirement benefits just got cut, but it doesn’t mean your benefits have to shrink too (more on that later). Effective May 1, the U.S. government adopted rules that will bar the "file and suspend strategy" for people born after April 30, 1950, putting an end to a unique strategy for drawing Social Security that helped many retirees boost their lifetime benefits significantly.

Two strategies designed to maximize Social Security retirement benefits just got cut, but it doesn’t mean your benefits have to shrink too (more on that later). Effective May 1, the U.S. government adopted rules that will bar the "file and suspend strategy" for people born after April 30, 1950, putting an end to a unique strategy for drawing Social Security that helped many retirees boost their lifetime benefits significantly.

The rule-making didn’t stop there either. The government is also putting an end to the "restricted application" strategy for receiving benefits, but not for everyone – if you were 62 or older as of January 1, 2016, you can still access this strategy. We’d encourage you to read our previous post here to review the details of how this strategy works, but the basic premise is that the spouse with the larger Social Security benefit would essentially ‘activate’ their benefit, and the other spouse would use a ‘restricted application’ to start receiving the spousal benefit. In the meantime, the person who claimed the spousal benefit would actually have their own benefit growing at the set annual rates for Social Security benefits. Once that spouse ‘activates’ their own Social Security benefit, it would be for a larger amount.

There’s One Strategy That Didn’t Get Banned – But Still Works Great

Even though a couple of strategies are getting legislated away, there is still the ‘old trustee’ method for maximizing your Social Security Retirement Benefits – just wait longer.

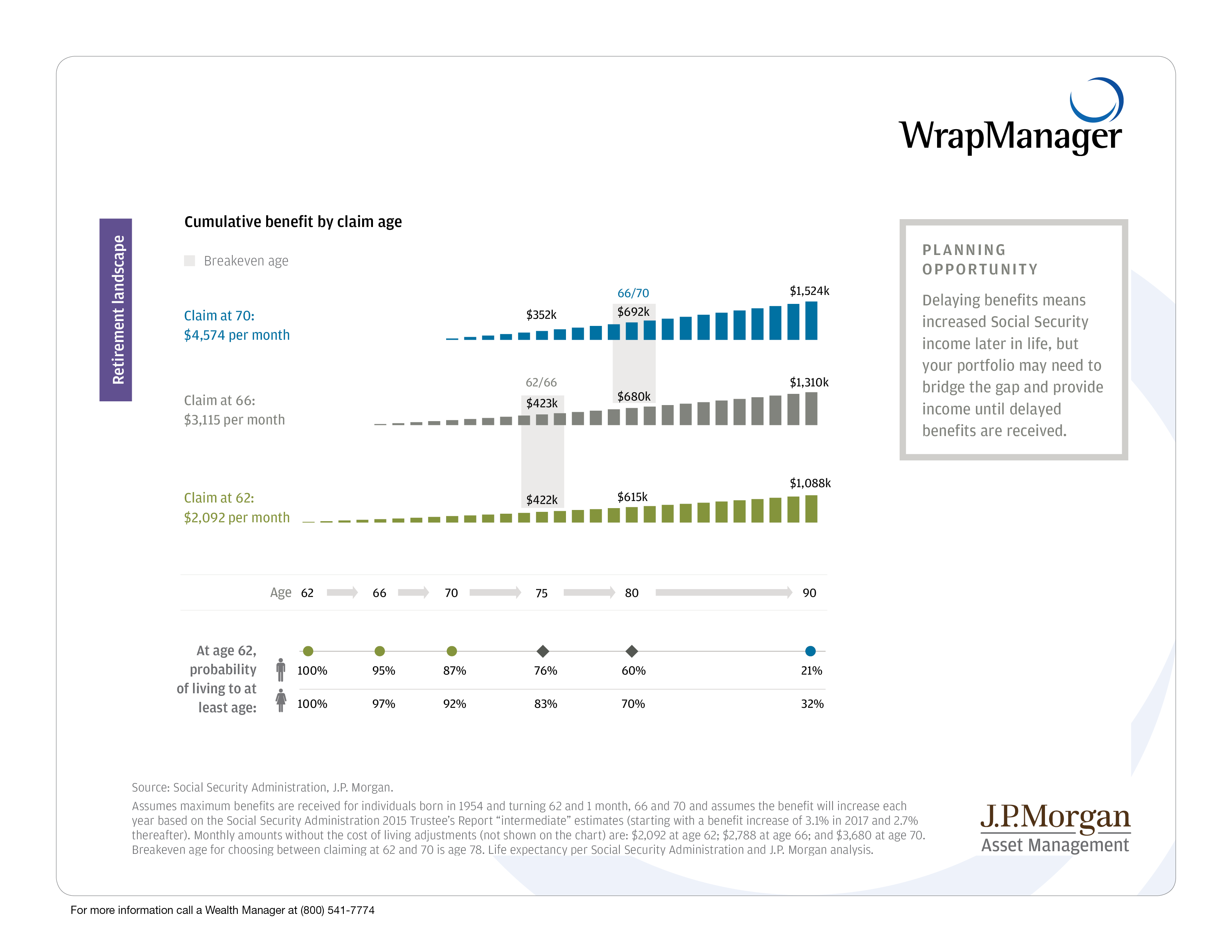

The longer you wait to claim your benefits, the larger your lifetime benefit could be, especially if you live a long, healthy life (which people are increasingly doing). JP Morgan created a graphic that spells it out pretty clearly. The retiree that can wait until age 70 to claim their Social Security would mathematically receive close to $500,000 more in payments than the person who claims at age 62 (assuming they both live to age 90). Think about how significant 500,000 extra dollar would be to your retirement plan! It’s huge.

A recent article in U.S. News & World Report laid out 4 criteria that can help you determine if you can delay taking your Social Security Retirement Benefits:

- You intend to continue working well beyond age 62

- You can use income from work or other sources to provide for your cash flow needs until your late 60’s or beyond

- You and your spouse enjoy good health

- You have a history of longevity in your family (or your spouse does)

If these conditions apply to you, then it could be worth considering delaying taking your Social Security benefits as long as possible, the ‘old trustee’ strategy for maximizing your lifetime benefits.

Talk to a Wealth Manager about Your Social Security Retirement Benefit Options

Recent legislation has narrowed your options for receiving Social Security benefits, but that doesn’t mean it has eliminated all of them. For many, the “restricted application” strategy still applies, and there are other options to explore when making this important financial decision. Don’t do it alone – call one of our Wealth Managers to evaluate your options and discuss how Social Security fits into your overall investment plan. You can reach us at 1-800-541-7774 or send us a quick note to wealth@wrapmanger.com.